Coverage Meaning Job – Commercial General Liability Insurance (CGL) is a type of policy that pays attention to business for physical injury, personal injury, and damage to property derived from the operations, products or injuries of the business occurring in the business building.

Commercial general liability insurance is considered a comprehensive business insurance, although it does not cover all the risks of liability that a business might face.

Coverage Meaning Job

Commercial general liability policies have different levels of attention. Policy may include building provision, which protects the business from allegations that occur on the physical location of the business during regular business operations. It may also include attention for physical injury and damage to properties that are the result of a finished product or service made in another location.

Pilot Randomized Controlled Trial Of Icanwork: Theory-guided Return-to-work Intervention For Individuals Touched By Cancer

Commercial insurance companies also sell too much attention to liability, which can be purchased to pay claims that exceed the CGL policy limit. Some commercial accountability policies may have exclusions limiting what steps are included. For example, a policy may not cover the costs associated with product recall.

When purchasing commercial general liability insurance, it is important for the business to distinguish a policy made by claims and incident policy.

A policy made by claims provides attention whenever a claim is made, no matter when the claim event occurred. An incident policy covers claims where the claim event occurred during the policy time, even if the policy has now ended.

In addition to commercial overall accountability policies, businesses can also purchase policies that provide attention for other business risks.

How Can I Get Health Insurance If My Employer Doesn’t Offer It?

For example, the business can purchase the accountability of employment practices to protect itself from allegations associated with sexual harassment, wrongdoing, and discrimination. Cyber insurance protects businesses from financial losses due to cutting data and similar attacks. It may also purchase insurance to cover errors and omissions made in financial reporting statements, as well as comment for compensation, arising from the actions of its directors and officers.

A typical commercial general insurance policy includes accidental damage or injuries but does not deal with intentional or expected injuries.

Depending on its business needs, a company may need to name companies or others as “additional insured” under its commercial liability insurance policy. This is common when businesses enter into a contract with another entity.

For example, if a car repair garage goes into a contract with ABC Co. To get the last to provide cleaning services for its facility, ABC Co. requires the owners of the garages to add ABC Co. as an “additional insurer” on its commercial general liability policy.

Types Of Employee Benefits: 17 Benefits Hr Should Know

In each of these cases, a commercial overall liability policy could cover the cost of hiring solicitors to protect the company or the cost of settling the claims. If a business has frequent claims against its CGL insurance, the insurer could charge the policy premium costs.

Commercial general liability insurance includes injuries to a person or damage to property occurring on a business building. CGL policies pay claims of property damage, personal injury (such as libel or slander), physical injury, and advertising injury.

Most CGL policies do not cover the deliberate or expected damage from the insurer. They also do not deal with compensation due to drunkenness (in alcohol -related businesses), pollution, automobiles or other vehicles, damage to business work, or additional obligations that the insurer could take. A business involved in these types of risks should purchase additional insurance for full attention.

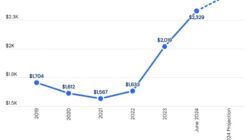

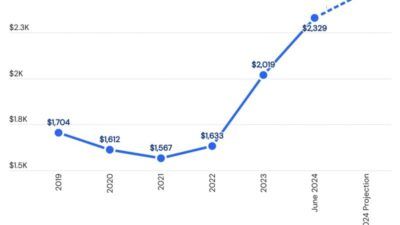

The cost of commercial overall liability insurance depends on the size of the business insured, the risk of its business operations, and the amount of attention needed. Some insurers say their clients pay between $ 300 and $ 600 for a million dollars of insurance. Others say their clients could pay as much as $ 1, 000.

What Is A Cover Letter? (and What To Include In One)

The insurer includes an insurer named (as an individual or business) specified in the insurance contract. The insurer named is usually the policy holder. The policy owner can also name additional insurers (as contractors) and additional named insurers (as fellow owners).

You can protect your business from a variety of risks, including the risk of a legal case arising from everyday business activities, with the purchase of a commercial overall accountability policy. CGL policies pay for property damage, physical injury, and other types of claims. This comment will help you pay attorney fees or settled costs in the event of a legal proceedings. And you can add to your attention with extensions that deal with errors and omissions, excessive liability, or employment practices liability.

You can’t predict what will happen in the future, but you can cover your business and reduce your risk with CGL policy.

Requires authors to use primary sources to support their work. These include white papers, government data, original reports, and interviews with industry experts. We also refer to original research by other respected publishers where appropriate. You can learn more about the standards we follow in producing accurate, impartial content in our editorial policy.

Graduation, Moving, New Job, Growing Family—big Moments Can Mean Big Changes! Make Sure Your Coverage Keeps Up. ✅ #milestones #lifeevents

The proposals appearing in this table come from compensation partnerships. This compensation can affect how and where listings appear. It does not include all the offers available in the market.

Best Small Business Insurance for August 2025 Best Food Truck Insurance Companies 2025 Longshore and Harbor Compensation Act Valuable Marine Policy: What it is and how it works vehicle and insurance paid to (CIP): Definition and examples of model policy holders: what it is and how it works operations insurance completed completed operations insurance

Inchmare clause: What does it mean, how does it work the American Land Title Association (Alta): What is it and how it works Business Automobile (BAP): What is it and how does it work buy an older home? Homeowners insurance is not the only thing to get – you probably need the professional liability insurance of home warranty contractors: Definition and attention of net amount at risk: what is it and how it works a premium to a surplus ratio: what is it, how it works, and the importance of living in one of these provinces? Do not make this mistake and expensive before a Vacationa insurance certificate shows that insurance policy is active and breaks down its main features, including conditions.

An insurance certificate (COI) is a document issued by an insurance company or broker. The COI confirms that an insurance policy is in place and outlines its terms and conditions. For example, a standard COI lists the policy holder name, the effective date of policy, the type of attention, policy limits, and other important details of the policy.

Medicaid Requirements In Ca

Without COI, a company or contractor will have difficulty securing clients as they will probably not want to take the risk of any costs that may be incurred by the contractor or provider.

Insurance Certificates (COIS) are used in situations where significant accountability and losses are of concern and requires COI, which in most business contexts. Insurance certificate is used for insurance testing.

Small business owners and contractors often have COI who prove they have insurance that protects from accountability for accidents or workplace injuries. When you buy liability insurance, the insurance company will usually provide an insurance certificate.

Without COI, a business or contractor owner can have difficulty winning contracts. Because many companies and individuals are hiring contractors, the client wants to know that a business owner or contractor has a liability so that they take no risk if the contractor is responsible for damage, injury or lower -standard work.

The ‘big Beautiful Bill’ Could Lead To Millions Losing Health Insurance

A company hiring a contractor or other entity for services should have a copy of their COI and ensure it is current.

Typically, a client will request a certificate directly from the insurance company rather than the owner of the business or contractor. The client should confirm that the insurer’s name on the certificate matches exactly to the company or contractor they are considering.

The client should also check the policy coverage dates to ensure the effective date of policy is up to date. The client should secure a new certificate if the policy is about to expire before the contracted work is completed.

Insurance certificates include separate sections for different types of accountability coverage listed as general compensation, auto, umbrella, and employees. The term “insured” refers to the policy holder, a person, or a company that appears on the certificate as being under the insurance.

4 On 2 Off Shift Pattern Explained: How It Works, Pros And Cons & Implementation Tips

In addition to coverage levels, the certificate includes a name, the policy holder’s mailing address, and describes the operations that the insurer performs. Insurance company address is listed, along with contact information for the insurance agent or insurance agency contact person. If several insurance companies are involved, all names and contact information are listed.

When a client requests COI, they become a certificate holder. The client’s name and contact information appears in the lower left corner, along with statements showing the insurer’s obligation to inform the client of policy canceling.

The certificate briefly describes the insurer’s policies and limits provided for all types of attention. For example, the General Liability section summarizes the six ends that the policy proposes by category and indicates whether the comment applies per claim

Full coverage insurance meaning, collision coverage meaning, dwelling coverage meaning, insurer affording coverage meaning, insurance liability coverage meaning, bumper to bumper coverage meaning, lapse in coverage meaning, cobra coverage meaning, comprehensive coverage meaning, no fault coverage meaning, pip coverage meaning, full coverage meaning