Technology Readiness Level Scale Applied By The Iea – Historically, research and innovation have been the bread of the Department of Energy and butter, but with the global time climbing and climate technology in a critical inflection, it is “deploying, deploying”.

The DOE restructured last year to better collaborate with the private industry, going from research and development (R&D) to demonstration and deployment (D&D). [The guide of our founder A DOE provides a startup roadmap that participates with the programs and opportunities of the Department.

Technology Readiness Level Scale Applied By The Iea

When it comes to fulfilling the ambitious goals of decarbonization of the Biden administration, the name of the game is “public-private collaboration”. And, as the DOE led the public sector’s efforts, the leaders of their numerous offices decided to put everyone on the same page. That is, the same more than 250 pages.

A) Schematic Diagram Of Technology Qualification Method By Dnv (b)…

After months of discussion with the private sector, the DOE presented its “ways to commercial elevation” on Tuesday, explaining the current state, the challenges and potential ways to “lift” for climatic technologies, initiating the storage of hydrogen, nuclear and long -term energy.

As David Crane, director of the Energy Demonstrations Office (OCED), says, this is an “first informative approach” of Doe to accelerate the commercialization of new essential net energy technologies.

“The industrial strategy of clean energy will be aimed at the private sector, enabled by the government,” said Jigar Shah, director of the Office of Loan Programs. “These reports are used as a resource aimed at informing decision -making in the industry, investors and the broadest community of the interested parties, and reflect the challenges and optimism of the private sector that assign capital to these sectors.”

DOE elevation reports intend to serve as “living documents” that monitor the demonstration and deployment of climate technology, based on a continuous commitment between the public and private sectors.

Demand-pull Tools For Innovation In The Cement And Iron And Steel Sectors

We sat with Vanessa Chan and Lucia Tian of the Office of Technology Transitions to break down the call for reports: Here are the barriers. Now let’s unlock them.

With the trifect of United States climate legislation and innovation and record investment, climate technology ecosystem is ready for commercial elevation.

The three reports that DOE shared this week cover long -term energy storage, clean hydrogen and advanced nuclear (with a breakdown of carbon management soon).

Net hydrogen opportunity: Net hydrogen production in the United States could grow from <1 m of metric tonnes a year ~ 10m of tons by 2030. Most short -term domestic demand will come from the existing end users (for example, ammonia) that replace the intensive carbon H2 with clean hydrogen. Space players say they are in a good position to quickly learn and reduce this technology to the cost curve. Transportation will be essential to ensure that H2 distributed use cases take off. The industry will also have to climb the electro -supply supply chains, the CO2 distribution and the storage infrastructure and a qualified labor force. PTC credits can support the creation of the offer side and doe start to think creatively about how to catalyze the side of demand with the existing funding.

Crucial Decade Ahead For The Future Of Rail

LDES- Opportunity: By 2060, the U.S. grid may need 225-460 GW of LDES capacity to support a zero clean economy. In the next five years, they will require an approach to planning (for example, labor formation, tax reductions or loans for manufacturing facilities) .- Challenges: To compete with LI battery breakthroughs, the solutions Les will have to quickly improve performance and markets will have to begin to compensate for the value of the LDES project, which is not today.

Advanced Nuclear Opportunity: Develop advanced nuclear technology could climb the American capacity of ~ 100 GW by 2023 to ~ 300 GW in 2050.- Technology: In short-term designs, GEN III+ SMR can see that the largest adoption, which could follow gene IV reactors.- Cost: The cost of building a nuclear project needs to fall dramatically. Recent nuclear construction projects in the United States have cost more than $ 10,000 per kW. After 10-20 deployments, advanced nuclear projects should go down to ~ 3, $ 600 per kW to unlock the deployment at Scale.- Timeline: rather better for nuclear. The initial deployment by 2035, instead of 2030, means that the industry should build an additional 20 GW and spend up to 50% more to reach the same deployment at 200 GW for 2050.- Challenges: shortly, on risk and credibility. The creation of this committed orders could be accelerated by means of the demand for aggregate utility, the cost of cost of cost (public or private) and the government that acts as an owner or office.

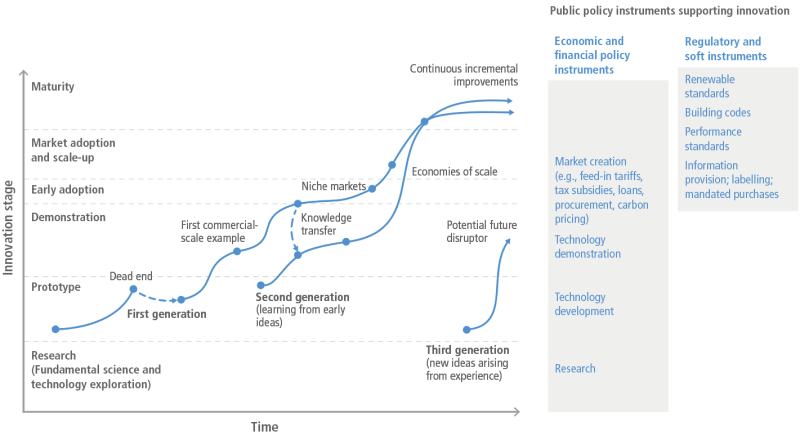

Founders, investors and DOE know all levels of technology preparation (TRLS), but technology is only a dimension of risk on the path to commercial lifting.

To establish the new standard for commercial adoption, the DOE created the adoption adoption levels (ARLS): a check list frame that considers factors such as costs, supply chains, regulations and market acceptance.

Trl Technology Readiness Level Developement-stages-trl-mrl-irl

Within these four areas there are 17 subcategories, which are scored individually as a low, medium or high risk. When composing the number of medium and high risk dimensions and map them in an array, you will get an ARL score of 1-9, which does not reflect not only the maturity of technology as TRLS, but also the market conditions needed for commercial adoption.

More consideration of the industry, instead of innovation, is a change in thought in Doe that goes beyond these reports. The offices throughout the department incorporate ARL into their processes and decision -making.

We talked to Vanessa Chan, marketing manager and director of the Office of Technology Transition (OTT), about the provision of their private sector experience in Doe and how they expect companies and investors to use Marc Arl and uprising.

How did the idea of elevation reports originate and why DOE decided to share them in this type of format?

Pdf) Assessment Of Classes Of Cdr Methods: Technology Readiness, Costs, Impacts And Practical Limitations Of Biochar As Soil Additive And Beccs

Spending the last twenty years doing marketing, one of the things I have found is that we are often very “technological push” [vs. Market shot]. At McKinsey, where I directed innovation practice, we were working with large companies spending billions of dollars on R&D, asking the question: “What does it prevent our technology from going through the door?” Many of them had to do with things like regulatory risks, the value proposal, the cost structure.

My job as a marketing director and director of the Office of Technology Transition (OTT) is to promote the application of the private sector of clean energy technologies. If you think of the different risk profiles throughout the RDD and D continuum (research and development, demonstration and deployment), we need the whole private sector that works together to bring us.

We did well as a nation in semiconductors. We have reached Moore’s law, where we doubled the number of transistors in a chip every two years. A single player could not do it on its own, so S Queatech gathered a commercial roadmap for the entire ecosystem to follow. When you market hydrogen or LDS, there are so many technologies. It’s not that simple. But this was inspiration: How do we get an ecosystem catalyzed everyone on the same page? What are the assumptions and shared data that people think?

Through bil, anger and chips, we now have $ 500 million to boost the clean energy transition. This was a natural place for OTT to work closely with the Net Energy Demonstrations Office (OCED), which has a lot of money out of bile, as well as the Loan Program Office (LPO). Because what we want to find out is how its resources can be used to mitigate the risks of climate technology to a point where the private sector feels comfortable to collect the ball and market? How do we take these $ 0.5 trillion to activate $ 23 trillion in the private sector?

Technology Options And Policy Design To Facilitate Decarbonization Of Chemical Manufacturing: Joule

To do it, we must put on the same page on what is required. Everyone is excited but wants to be a fast follower. If we are all fast followers, nothing will happen. I think people are waiting right now and we really can’t wait.

They are all critical of achieving our goals for clean energy transition. You cannot achieve the energy goals that this administration has without nuclear, because it is a constant energy